The Statute Staple in Early Modern Ireland

Published in Early Modern History (1500–1700), Early Modern History Social Perspectives, Features, Issue 4 (Winter 1998), Volume 6

Reconstruction of the Seal of the Staple of the City of Dublin. (Robert Gordon, Rainnea Graphics)

The Irish staple, which dated from the thirteenth century, was initially established to regulate the trade of basic, or staple, goods such as wool and hides which could only be sold to foreign merchants in designated ‘staple’ towns—originally Dublin, Waterford, Cork and Drogheda. It also provided a sure way for traders to recover their debts. By the early seventeenth century the real significance of the staple lay not in the co-ordination of trade but in the regulation of debt and the creation of a sophisticated credit network. Perhaps in recognition of this the Irish staple towns expanded to include Belfast, Carrickfergus, Derry, Galway, Kilkenny, Limerick, New Ross, Sligo, Wexford, and Youghal.

How the staple worked

The brethren and merchants of the staple elected—for the period of a year—a mayor, who enjoyed considerable legal powers especially in the regulation and recovery of debt, and two constables of the staple. Among other things the mayors of the staple were empowered to take recognisances of debt incurred on the staple. The recognisances, known as statutes staple, were a form of registered bond by which the debtor(s) entered into a recognisance to pay the creditor(s) a fixed sum, at a given time, together with interest at 10 per cent. The amount of the bond was not a record of the actual loan but security for the loan and was usually double the amount of the loan. Three registers, covering the years 1596-1637 and 1664-78, recording the entry of bonds on the Dublin staple are extant and are housed in the Dublin Corporation Archive. These volumes are all in reasonable condition and apart from two principal exceptions (May-October 1604 and August 1615-August 1616 when no transactions were recorded) appear to be remarkably complete with transactions being regularly conducted throughout the course of the year. Unfortunately no staple books appear to have survived for the staple towns outside Dublin and the amount of business transacted on the provincial staples, especially Cork and Limerick, could have been very considerable indeed.

If a debtor defaulted on repayment and he lived within the jurisdiction of the staple town, the mayor had the power to imprison him or to take possession of his moveable goods and his lands and to use them to repay the creditor. However, in many cases, especially if the debtor lived outside the jurisdiction of the staple, the clerk of the recognisances certified the debt in to the Court of Chancery. After certifying the debt into Chancery, the creditor then delivered a writ to the sheriff of the county in which the debtor’s lands lay (the acknowledgement of a debt contained in a recognisance of statute staple was the judgement itself). The sheriff seized the debtor’s property (after impaneling a jury to appraise its value) and returned an inquisition into Chancery. A writ of liberate was then issued in Chancery to the creditor which instructed the sheriff to release the debtor’s goods and lands to him in fulfilment of the debt. Five registers of bonds, kept by the clerk of recognisance of the Chancery between 1618 and 1687, were bought by the British Library in the mid-nineteenth century and are housed there. These Chancery volumes are particularly interesting because they contain a wealth of detail on the activity of all of the Irish staple towns. The greatest number of entries recorded in Chancery came from Dublin (66 per cent), then Cork (13 per cent), Drogheda (7 per cent), Limerick and Carrickfergus (4 per cent each), Kilkenny and Galway (1 per cent each) with the least coming from Londonderry (only two transactions or 0.15 per cent of the total).

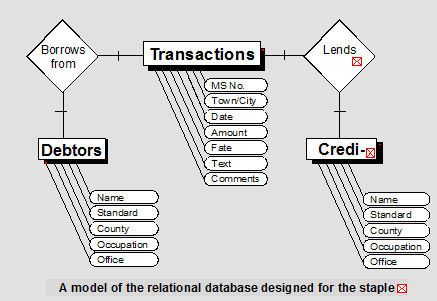

The Statute Staple Database

Between them these eight volumes record 4,000 individual transactions (2,600 on the Dublin Staple and 1,400 in the Chancery volumes). Virtually every entry lists the status or occupation of the debtor(s) and creditor(s), often with the office they held. The address of the debtor(s) and creditor(s) was also listed, together with the date on which the transaction took place and the amount of the bond. A considerable number of individual transactions were also annotated in the margins. The Chancery volumes included lengthy memoranda and indentures of defeasance that outlined a repayment timetable and occasionally indicated why an individual wanted to borrow money in the first place. In the Dublin staple books these annotations stated whether a case was referred to the Court of Chancery or to the local sheriff and whether the bond was cancelled and the money repaid.

The important information contained in these transactions has been extracted and entered under a variety of ‘field’ headings in a relational database. In all over 10,000 names—4,309 creditors and 5,879 debtors—were entered into the database. Predictably the same person appeared more than once and so the actual number of people using the staple was probably between 5,000 and 6,000. The names of hundreds of Irish merchants, landowners, tradesmen, aristocrats, municipal officials and government officers, and the names of scores of widows and clerics (including bishops from nearly every diocese in Ireland) were recorded. In fact the names of individuals lending and borrowing on the Irish staples read like a veritable ‘Who’s Who’ of early modern Irish history and embrace every ethnic and religious group living in Ireland. They included the Earls of Ormond, Orrery, Antrim, Clancarthy, and Inchiquin; leading government officials—Sir John Davies, Sir William Petty, and Richard Cox; Catholic confederates—Lord Conor Maguire, Sir Phelim O’Neill, Richard Bellings, and Patrick Darcy; and the antiquarians, Mathew DeRenzy and Sir James Ware. Colourful characters also appear such as Valentine Greatrakes, the ‘touch doctor’ from County Waterford, and Thomas Blood, who tried in 1663 to assassinate the Duke of Ormond and in 1671 to steal the crown jewels.

Political and economic crisis

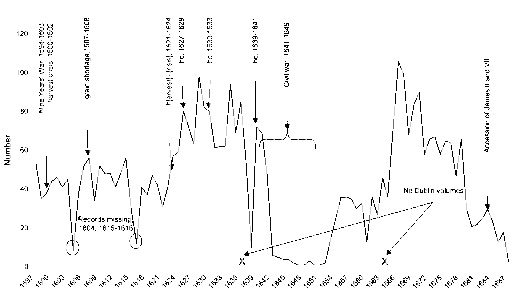

The total number of transactions that were recorded in the extant staple books has been plotted on a line graph (overleaf) that clearly demonstrates the relationship between staple activity and economic and political crisis. For example, the impact of harvest failure and the intermittent subsistence crises, especially of the mid-1620s and late 1630s when the availability of Irish land was at a premium, appears to result in an increase in the activity of the staple as people, deprived of their landed revenues, turned to the staple for credit. The outbreak of war after 1641 had a dramatic and devastating impact on the operation of the statute staple throughout Ireland. It provoked a major national economic crisis and fundamentally undermined the networks of trust and mutual interdependence that sustained the staple as an effective paper credit system. As a result Dublin appears to be the only city to operate a staple at all during the 1640s.

Dublin served as the nation’s financial capital throughout the seventeenth century and, with the principal exception of the 1640s, debtors and creditors travelled from every county in Ireland to use the Dublin staple. Nearly 3,000 individuals lent money on the Dublin staple; 82 per cent originated in Leinster (58 per cent with Dublin addresses); the remaining 18 per cent originated from every other county in Ireland (4 per cent from Munster, 3 per cent from Connacht and 5 per cent from Ulster) and from England and Scotland (4 per cent). Roughly 4,100 individuals borrowed money on the Dublin staple: 76 per cent originated in Leinster (35 per cent with Dublin addresses); 8 per cent in Ulster; and 7 per cent each in Munster and Connacht. They highlight the importance of Dublin as a commercial centre, not simply as a source of credit for people resident in Ireland but for debtors from England and Scotland as well. For instance, between 1619 and 1685 six Scots borrowed £5,510 on bond on the Dublin staple, invariably from kinsmen who had been involved with the Ulster plantation. A further eight debtors gave an English address.

How much were these debtors actually borrowing? The total value of bonds recorded on the Dublin staple amounted to nearly £1.5 million. The average bond was for £560 and the largest bond recorded on the Dublin staple was for £10,640. The amounts of money borrowed on the Dublin staple almost quadrupled between 1597 and 1636. In the years after the restoration the amounts transacted remained fairly constant, though the average size of individual bonds increased significantly from £455 to £1,029. The total value of bonds recorded in the Chancery volumes amounted to £1.2 million: the largest bond was for £20,000 and the average size of individual bonds was roughly £900.

Creditors and Debtors

In social and economic terms credit was a levelling force within the community and reciprocal bonds of indebtedness bound rich and poor alike irrespective of ethnicity or religion. A preliminary analysis of the staple records indicates that individuals from a wide variety of social and economic backgrounds—members of the Irish aristocracy, the gentry, merchants, soldiers, farmers, tradesmen, craftsmen, clergymen, civil and government officials, and women—made extensive use of the staple.

By far the most important creditors were members of the landed gentry (who described themselves as ‘knights’, ‘baronets’, ‘esquires’, ‘gentlemen’ and ‘gentlewomen’). Why did they lend money and to whom? What was the source of the cash or credit they loaned and what amounts were involved? What was the religious and ethnic origin of these landed creditors and of their debtors? To what extent did lending habits change over time? It may not be possible to answer all of these questions in full. However even a cursory analysis of gentry creditors suggests that they used the staple as a means of increasing their landed bases, of supplementing their incomes through money lending, and of helping out friends and kinsmen.

The lending habits of the gentry appear to have changed over the course of the century. During the early decades gentry creditors originated from virtually every county in Ireland and from all ethnic and religious groups. Over time the number of native gentry creditors decreased sharply throughout the country, but especially in the western seaboard counties and in Counties Wicklow, Carlow, Waterford, Tipperary and Kilkenny. After 1660 the greatest number of gentry creditors were to be found in Counties Antrim, Down, Meath, Kildare, King’s County, Limerick, Cork and, above all, Dublin. These individuals appear to have included substantial numbers of Old Protestant entrepreneurs together with speculators who had acquired lands during the 1650s.

The Colvills serve as an excellent example of an Old Protestant gentry family that made extensive use of the staple during the later seventeenth century. Alexander and Robert Colvill, prominent local officials and landowners with estates in Counties Antrim and Down, were eager to build up their estates by lending money to individuals who, desperate for cash, had no alternative but to mortgage their lands. Over a period of thirty years (1655-1685) father and son, using the staples in Dublin and Carrickfergus, lent at least £46,000 on bond (since most of these transactions were recorded in the Chancery volumes the total amount that they lent probably greatly exceeded this figure). With only one exception, they lent to local men, often of considerable importance: Sir John Clotworthy, later Lord Massareene; Arthur Chichester, Earl of Donegal; Sir George Rawdon; and Hugh Montgomery, Earl of Mount Alexander (he borrowed c. £15,500 in a single year, 1675). Their other debtors included planters, many of whom had settled in East Ulster during the early seventeenth century (John Edmunston, John Shaw and the Rowleys of Londonderry) or had served as army officers during the 1640s and 1650s (John Galland). In only one instance, that of the O’Haras of Cregbilly, with whom they had intermarried, did the Colvills lend to native Catholic families. The absence of native debtors is striking and this no doubt reflects the changing nature of land ownership in East Ulster during the later decades of the seventeenth century.

Merchants and civic patricians also served as important sources of credit. Between 1597 and December 1679, 104 aldermen, from Cork, Galway, Limerick, Drogheda and, above all, Dublin, lent on bond £191,602 (only forty-four borrowed money). These aldermen, who appear to have had ready access to sources of cash, of credit, and possibly of goods, served as vital sources of credit for farmers and small landholders as well as tradesmen throughout Ireland. The same held true for merchants. Of the 780 creditors who gave their occupation as ‘merchant’, 62 per cent originated in Dublin (roughly seven per cent came from Drogheda, Cork, and London). They included the Allens, Arthurs, Brices, Dowds, Flemings, Frenchs, Kennedys, Mapas, Purcells, and Usshers. With a little effort it will prove relatively straightforward to reconstruct the financial fortunes of these merchant families, to untangle the webs of indebtedness in which they enmeshed themselves, and to determine whether they used the statute staple as a means of acquiring landed estates and accumulating cash through money lending.

From the perspective of the creditor—whatever their status or occupation—the staple provided reasonable security for any loan in that the bond the debtor signed usually amounted to twice the amount of the actual debt while the debtor’s lands served as ultimate collateral. Moreover the staple offered the creditor easy access to the law in the event that the debtor defaulted. The reluctance of English moneylenders to accept Irish land as collateral also ensured that these entrepreneurs enjoyed a captive market and received a return of 10 per cent on their investment. Given that interest rates of between 30-40 per cent were not unusual in the early seventeenth century (especially in the 1640s), this stable rate of interest, though high by English standards, also appealed to debtors.

Resolution of economic disputes

Clearly for any credit system to work effectively mutual trust between creditor and debtor was essential. To maintain their good reputation many debtors fulfilled their financial obligations on time. In a significant number of instances a debtor recorded the payment of a debt and had the bond declared void—14 per cent of bonds (306) concluded between 1597 and 1637 were apparently satisfied and this number rose to 25 per cent between 1665 and 1678. Other debts would have been cancelled without leaving any trace allowing the debtor to maintain his/her credit worthiness and to continue borrowing on the staple.

Other debtors did not fulfil their obligations forcing the creditor to resort to litigation, which appears to have been both reasonably efficient and relatively cheap. Between 1615 and 1637 the clerks of the Dublin staple issued 391 out of a total of 2,133 certificates (18 per cent) to Chancery; while between 1665 and 1678 they issued 106 out of 480 certificates (22 per cent) to Chancery. In other words nearly one fifth of all transactions recorded in the Dublin staple books, proceeded to the Court of Chancery in the early seventeenth century; while nearly one quarter were pursued in Chancery in the later decades. In ninety-nine cases the instigation of court proceedings prompted tardy debtors into paying or drawing up repayment schedules.

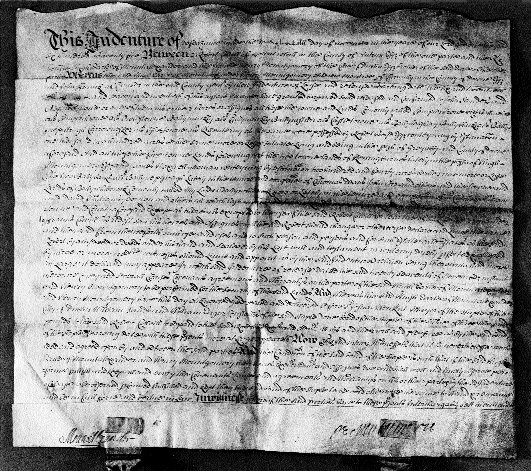

Sir Phelim O’Neill, later leader of the 1641 Rebellion, borrowed £1,000 on bond from Arthur Hill and the Solicitor-General, Sir Edward Bolton. The original transaction was recorded on the Dublin staple on 13 February 1639. (National Library of Ireland)

Despite attempts to improve the procedures whereby debts could be recouped and legal loopholes eliminated, recovering money became complicated if the creditor or debtor died, as many did, before the debt could be repaid or if the creditor assigned the bond to someone else. Matters became more perplexing still if debts were assigned to others, if the debtor or creditor had been on the losing side during the 1640s and if the estates of debtors had been confiscated. The staple records thus provide a rare insight into the complex processes of the resolution of economic disputes in seventeenth-century Ireland and, perhaps, pave the way for a wider study of the role the courts played in Irish economic life.

Limitations

While the staple records can illuminate patterns of borrowing and lending especially for individuals whose personal and estate archives have not survived, they do have their limitations. To fully understand the nature of indebtedness in seventeenth-century Ireland, especially what motivated debtors and creditors, the staple records must be interrogated alongside other relevant sources. Qualitative evidence—letters and above all diaries—provide valuable insights. The Earl of Cork’s diary, for example, bristled with references to his debtors whether they were his tenants, business associates or kinsmen. Many of the 1641 depositions included long lists of debts often amounting to thousands of pounds and Raymond Gillespie and Nicholas Canny have demonstrated the insight they provide to the importance of money lending and indebtedness at a local level in the pre-war years. Sadly the archives of Irish local and central courts have almost all perished. However early twentieth-century transcripts of the Chancery decree rolls (which deal largely with debts and mortgages) are extant in the National Archives in Dublin. The records of the Commissioners of the Court of Claims have also survived and contain numerous references to debts, including ones contracted on the staple. These are particularly useful since they indicated what lands stood as security for the bond.

Finally, estate records—where they survive—serve as an invaluable source for the study of debt since they often include lists of debts, promissory notes, different types of bonds, and details of mortgages. To cite but one example, the Percival papers, housed in the British Library, contain numerous deeds, mortgages, promissory notes and bonds (including those transacted on the staple). A detailed examination of these, in conjunction with the staple records, the 1641 depositions and extant court proceedings, will provide a unique insight into the lending and borrowing habits of an important and influential Protestant gentry family living in Munster.

Conclusion

‘Inadequate data [does] not become scientific information simply by virtue of being processed through a computer.’ The late Christina Larner’s cautionary ‘health warning’ originally aimed at overzealous scholars of seventeenth-century witchcraft applies equally to the Irish statute staple database. This database nevertheless offers historians, genealogists, and other interested scholars easy access to repetitive dry, legal records that were previously very difficult to interrogate and interpret. The database will never serve as a substitute for consulting the original staple volumes whether in Dublin or London, however it does bring together—for the first time—all of the early modern Irish staple books. Thus it enables interested scholars to access easily and to interrogate rigorously a wealth of information which has been shamelessly overlooked for far too long.

A staple indenture of defeasance between Robert Colvill and Earl of Mount Alexander for £3,000, transacted on the Dublin staple on 27 November 1675. (National Archives)

Much about the staple remains unknown and the precise mechanics of borrowing are often difficult to determine. Despite this the staple records serve as an invaluable—if often incomplete—guide to indebtedness and the social and economic history of seventeenth-century Ireland. In an economy where capital and coinage were particularly scarce, the staple served a very important function as a national paper credit system, albeit one centred on Dublin, which was accessible to men and women from a wide range of religious, social and economic backgrounds. However only by constructing ‘webs of indebtedness’ and by untangling the patronage networks in which they were embedded, especially at a local level, will the enormously complex credit systems operating in early modern Ireland and the land transfers—usually in the form of mortgages—which often accompanied them be fully understood. Given the number of people involved in these credit networks this will no doubt prove a lengthy task and one that will require historians, genealogists, and scholars interested in local and urban history to work together very closely.

Jane Ohlmeyer lectures in history at the University of Aberdeen

Further reading:

J. Ohlmeyer and É. Ó Ciardha (Eds.), The Irish Staple Books, 1596-1687 (Dublin Corporation 1998). The Staple Database has been published as an accompanying CD-ROM.